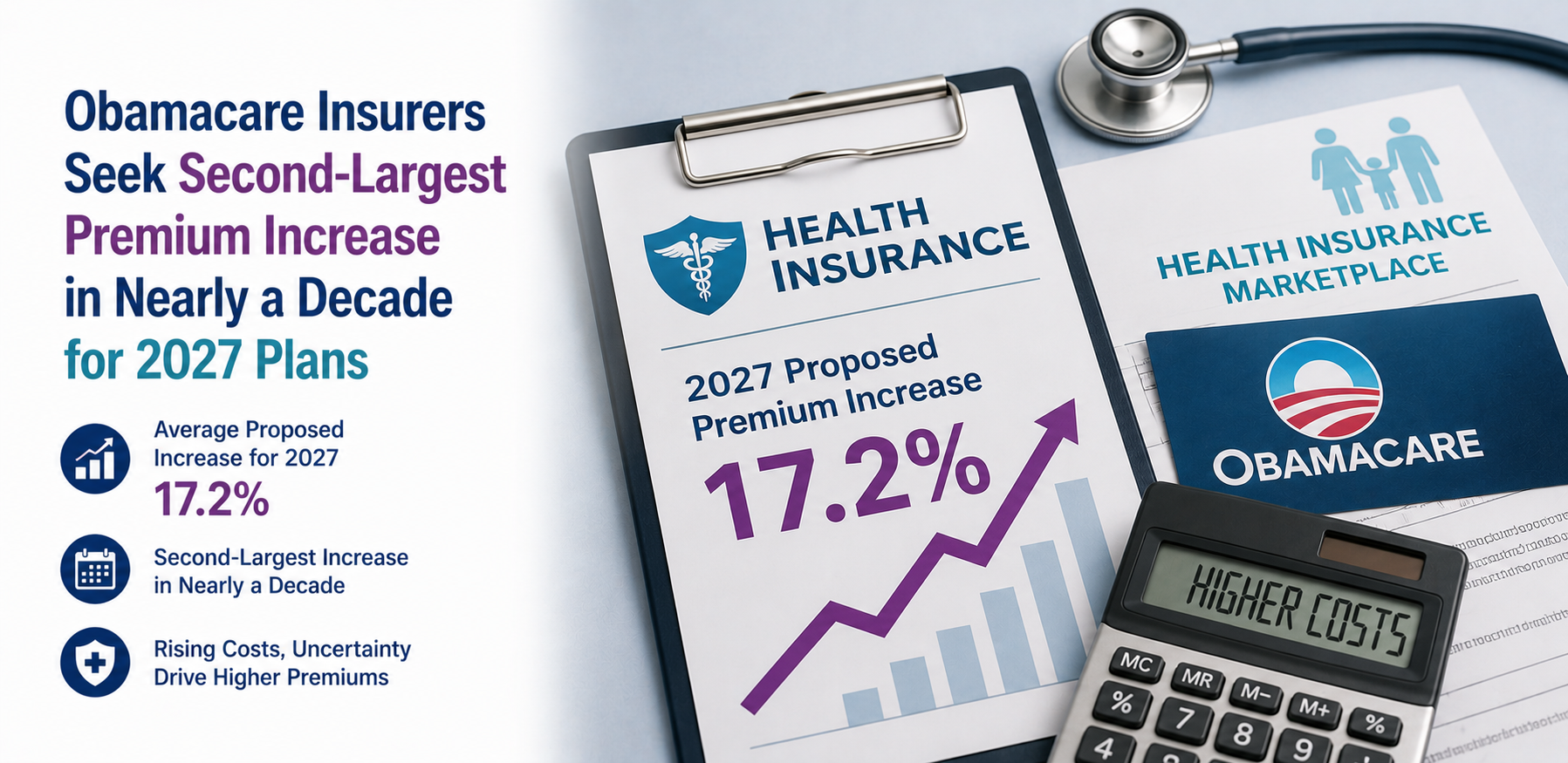

Obamacare Insurers Seek Second-Largest Premium Increase in Nearly a Decade for 2027 Plans

What's Happening

Health insurers offering coverage through the Affordable Care Act (ACA) marketplaces have requested an average premium increase that would be the second-largest in nearly a decade for health plans sold in 2027. According to early filings reviewed by Reuters, insurers cite rising healthcare costs, increased use of medical services, and uncertainty surrounding federal healthcare policies as key reasons for seeking higher premiums. (reuters.com)

The proposed increases are not final. State insurance regulators will review the requests over the coming months before approving, modifying, or rejecting the proposed rates. The final premiums consumers pay may differ from the initial filings.

The requests highlight continuing financial pressures across the U.S. health insurance market as insurers balance rising medical expenses with the need to keep coverage affordable.

What Is the Affordable Care Act Marketplace?

The Affordable Care Act (ACA), often called Obamacare, created online health insurance marketplaces where individuals and families can purchase private health insurance. These plans are designed primarily for people who:

- Do not receive insurance through an employer.

- Are self-employed.

- Retire before becoming eligible for Medicare.

- Need individual or family health coverage.

Many marketplace enrollees qualify for federal premium subsidies based on household income, helping reduce their monthly insurance costs. Millions of Americans now obtain health coverage through ACA marketplace plans each year.

Why Are Insurers Requesting Higher Premiums?

Insurance companies calculate premiums based on their expected healthcare costs for the coming year. Several factors are contributing to higher projected spending.

- Rising Medical Costs: Healthcare providers continue facing higher labor, supply, and operational expenses, increasing the overall cost of medical care.

- Greater Use of Healthcare Services: Insurers report that patients are making greater use of physician visits, hospital care, outpatient procedures, diagnostic testing, and prescription medications. Higher utilization generally leads to increased claims costs.

- Expensive Specialty Medicines: The continued growth of specialty drugs—including treatments for cancer, autoimmune diseases, and obesity—is placing additional pressure on insurer budgets. Many of these medications cost thousands of dollars per month.

- Policy Uncertainty: Insurers also cited uncertainty surrounding future federal healthcare policies and regulations, which can make it more difficult to accurately estimate future costs.

How Are Premium Rates Determined?

Every year, insurers submit proposed premium rates to state insurance departments. Regulators review these requests by examining medical cost projections, claims experience, enrollment trends, administrative expenses, and financial assumptions. State regulators may approve the requested increase, reduce the requested increase, request additional justification, or reject portions of the filing. As a result, the final approved premium changes often differ from the initial requests submitted by insurers.

Will Consumers Pay the Full Increase?

Not necessarily. Many ACA marketplace enrollees receive premium tax credits from the federal government. These subsidies adjust based on income and the cost of benchmark insurance plans. For many subsidized consumers, monthly premium increases may be smaller than the requested rate increases. Some consumers may see little change in monthly premiums. Others who do not qualify for subsidies could experience larger premium increases. The actual financial impact therefore varies depending on income, location, and plan selection.

Why Healthcare Costs Continue Rising

Premium increases reflect broader trends across the healthcare system. Major drivers include higher hospital costs, rising physician reimbursement, increased prescription drug spending, growth in chronic diseases, aging populations, more advanced medical technologies, and greater demand for healthcare services. Health insurers must account for these factors when pricing future coverage. As healthcare spending continues rising nationwide, premium adjustments have become a recurring feature of the insurance market.

What Happens Next?

The premium requests now enter the regulatory review process. Over the coming months, state regulators will examine insurer filings, companies may revise their proposed rates, and final premiums will be approved before the next enrollment period begins. Consumers will then be able to compare available plans during the ACA open enrollment period and determine which options best meet their healthcare and financial needs.

Industry Impact

- Health Insurers: Companies continue balancing rising medical costs with the need to maintain competitive insurance products.

- Healthcare Providers: Higher utilization and increasing medical costs continue affecting reimbursement and insurer spending.

- Consumers: Individuals purchasing coverage through ACA marketplaces may experience higher premiums, although many will continue receiving federal financial assistance.

- Policymakers: Premium filings provide an early indication of broader healthcare cost trends and may influence future discussions about healthcare affordability.

Why This Matters

The latest premium requests underscore the ongoing challenge of balancing affordable health insurance with rising healthcare costs. While insurers face increasing expenses from medical care, prescription drugs, and higher healthcare utilization, consumers remain sensitive to premium increases that can affect access to coverage. Because millions of Americans rely on ACA marketplace plans, even modest premium changes can have significant implications for household healthcare spending. The regulatory review process will determine how much of the requested increases are ultimately approved, but the filings reflect continued financial pressure throughout the U.S. healthcare system.

Key Takeaways

- ACA marketplace insurers requested the second-largest premium increase in nearly a decade for 2027 plans.

- Rising healthcare costs, increased medical utilization, specialty drug spending, and policy uncertainty are driving the requests.

- State regulators will review and may modify the proposed premium increases before they take effect.

- Many consumers receiving federal premium subsidies may experience smaller increases than the requested rates.

- The filings highlight continuing cost pressures across the U.S. health insurance market.

What This Means for Healthcare Marketers

The proposed premium increases illustrate the continued financial pressures affecting every part of the healthcare ecosystem. Rising medical utilization, specialty drug spending, and higher provider costs are influencing not only insurers but also healthcare providers, pharmaceutical companies, employers, and patients. Organizations across the industry are increasingly expected to demonstrate value while helping manage overall healthcare costs.

For healthcare marketers, affordability is becoming a central part of healthcare decision-making. As consumers face higher insurance premiums and out-of-pocket costs, messaging that emphasizes clinical value, cost-effectiveness, preventive care, and improved health outcomes will become increasingly important. Companies that can clearly communicate both medical and economic benefits are likely to be better positioned in an environment of growing cost sensitivity.

For healthcare intelligence teams, annual premium filings offer valuable insight into broader healthcare spending trends. Monitoring insurer rate requests, regulatory decisions, medical cost inflation, and utilization patterns can help organizations anticipate future market dynamics, reimbursement changes, and evolving payer priorities across the U.S. healthcare system.